Ever wondered why some insurance claims are approved in days while others take weeks?

For healthcare professionals, delays in claim processing aren’t merely administrative; they directly impact reimbursement timelines, workflow efficiency, and patient satisfaction. In 2024, nearly 38% of survey respondents reported that at least one in ten claims was denied. These bottlenecks not only slow processing but also increase pressure on revenue cycle teams to maintain cash flow and compliance.

In this blog, you will learn how long does health insurance have to process a claim, including federal and state timelines, payer practices, and technology-driven efficiencies.

TL;DR (Key Takeaways)

- Claims use ICD-10, CPT, and HCPCS codes to standardize data for billing, compliance, and analytics.

- ERISA timelines: urgent claims 72 hours, pre-service 15 days, post-service 30 days, with allowed extensions.

- Processing times vary: electronic claims, 7–14 days; standard claims, 45 days; paper claims, 30–45 days. Delays may arise from errors or missing information.

- Delays often result from coding errors, incomplete forms, high-value claims, high volumes, or missing documentation.

- Best practices: electronic submission, eligibility checks, accurate coding, claim tracking, denial analytics, and AI-assisted workflow.

Table of Contents:

- Understanding Health Insurance Claims and Their Role

- Federal Guidelines under ERISA for Group Health Plans

- Typical Timelines for Health Insurance Claim Processing

- How State Laws Affect Insurance Claim Timelines?

- Common Reasons Your Claim May Be Delayed

- How to Speed Up Your Insurance Claims Process?

- Best Practices for Healthcare Operations Teams

- Conclusion

- Frequently Asked Questions (FAQs)

Understanding Health Insurance Claims and Their Role

A health insurance claim is how a provider or patient requests payment from an insurer for medical services or treatments. Think of it as the bridge between care delivered and reimbursement received. Claims can be pre-service (requiring approval before treatment), post-service (submitted after care), or urgent (needing fast review due to medical necessity).

Each claim contains critical details, patient info, diagnosis codes (ICD-10), procedure codes (CPT/HCPCS), dates of service, and itemized charges. Accurate submission is crucial: errors can result in delays, denials, or additional follow-up. Claims also play a vital role beyond payment, supporting multiple critical functions in healthcare operations:

- Standardizing Data: Health insurance claims utilize codes such as ICD-10, CPT, and HCPCS to structure clinical and administrative information. This ensures accurate billing, reporting, and reliable datasets for analytics and population health management.

- Compliance and Auditing: Claims document services rendered, ensuring adherence to federal and state regulations, payer contracts, and internal policies. They support audits, inspections, and regulatory reviews, helping organizations avoid penalties.

- Financial Flow and Revenue Cycle Management: Properly processed claims ensure timely reimbursement to providers, maintaining cash flow and operational stability. They also help track costs, identify inefficiencies, manage accounts receivable, and support strategic financial planning for healthcare organizations.

- Operational Insights: Beyond immediate reimbursement, claims data can reveal patterns in service utilization, coding accuracy, claim denials, and payment timelines, enabling organizations to implement process improvements, reduce errors, and optimize the revenue cycle.

Understanding claims is essential for anyone managing the revenue cycle or ensuring compliance; it’s where clinical care meets workflow efficiency.

Federal Guidelines under ERISA for Group Health Plans

Under the U.S. federal law ERISA (Employee Retirement Income Security Act of 1974), there are defined timeframes for group health plan claims processing:

1. Urgent Care Claims

Must be processed as quickly as possible, and no later than 72 hours after receipt. If additional information is required, the insurer must notify the claimant within 24 hours, allowing at least 48 hours for the claimant to respond. A final decision must then be issued within 48 hours of receiving the information, or by the 72-hour deadline, whichever comes first.

2. Pre-Service Claims

Claims for services that require prior approval must be processed within a reasonable time, not exceeding 15 days. Plans may grant a one-time extension of up to 15 additional days if the claimant is notified before the original deadline.

3. Post-Service Claims

Claims submitted after services are rendered must be decided within a reasonable time, not exceeding 30 days. Extensions may be allowed if the claimant is notified in advance.

These timelines ensure timely decisions and protect participants’ access to necessary care under ERISA-regulated group health plans. Now, let’s see how actual practice and state-level rules can expand or tighten these expectations.

Typical Timelines for Health Insurance Claim Processing

While ERISA sets minimum timelines for group health plan claims, actual processing can vary depending on claim complexity, submission method, and insurer workflow. Understanding these variations helps operations teams anticipate delays and plan follow-ups more effectively.

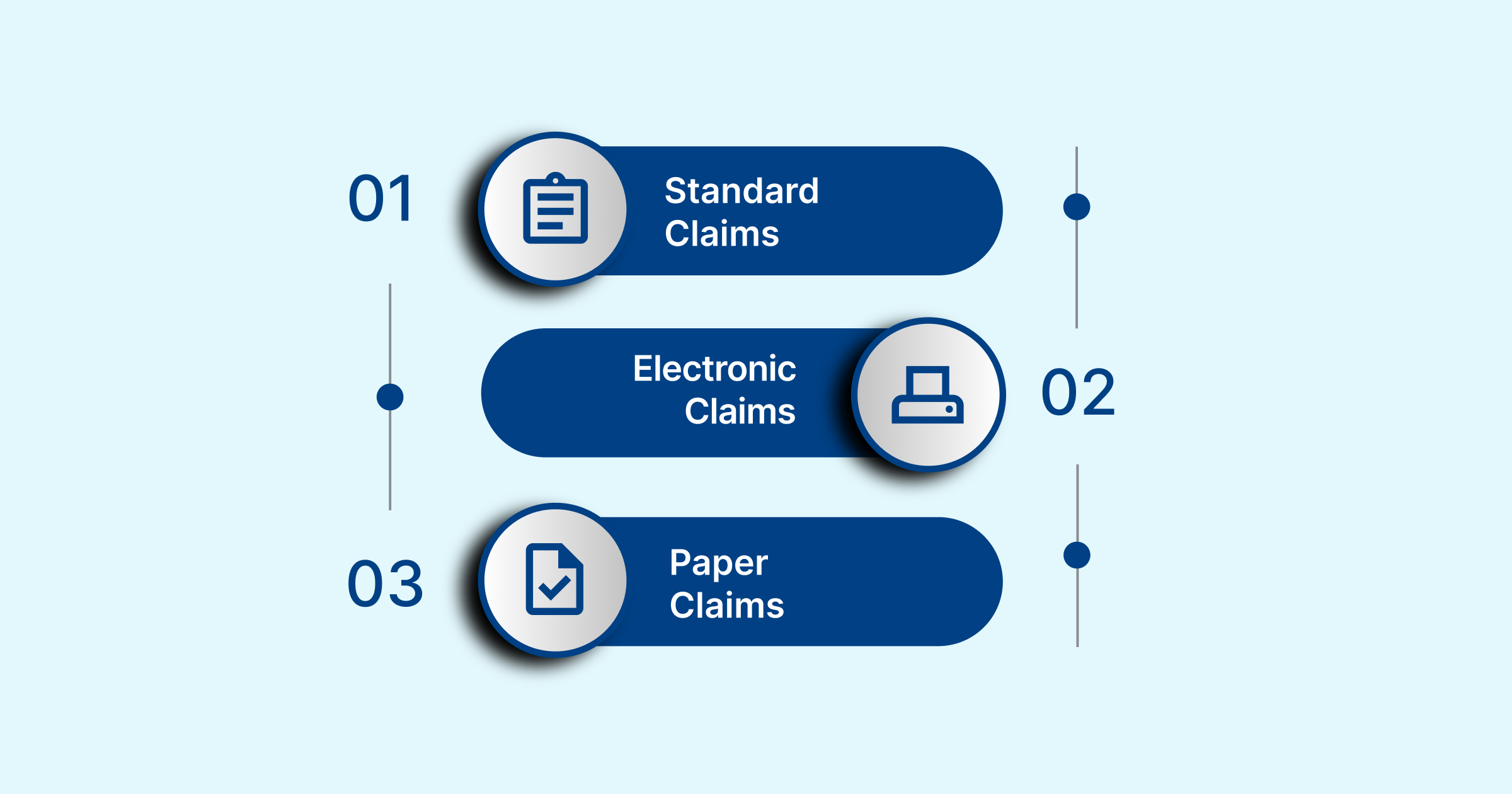

- Standard Claims: Most insurers aim to process claims within 45 days of receipt. However, the final Explanation of Benefits (EOBs), which details approvals, denials, or adjustments, may not reach patients for 3 to 12 weeks. Delays often occur due to audits, coordination of benefits, or requests for additional documentation.

- Electronic Claims (EDI): Submitting claims electronically speeds up the process. Automated verification and coding reduce errors and turnaround time, with most EDI claims processed within 7 to 14 days. This makes electronic submission the preferred method for efficiency and accuracy.

- Paper Claims: Physical submissions require manual handling, including data entry and document verification, which can extend processing times to 30 to 45 days. Paper claims are also more prone to errors, follow-up requests, and resubmissions, making them less efficient than electronic claims.

These variations highlight how errors in coding or documentation can lead to bottlenecks, delay reimbursements, and increase administrative costs. RapidClaims addresses these challenges by utilising AI to automate coding, clinical documentation, and denial prevention, achieving 98% clean claims, 40% fewer denials, and a 170% increase in coder productivity, helping healthcare teams streamline workflows and accelerate revenue cycles.

Considering these operational realities, let’s examine how variation across states and plan types introduces additional complexity.

How State Laws Affect Insurance Claim Timelines?

In addition to federal ERISA requirements, many states have their own rules that impact how group health plan claims are processed. These regulations may vary depending on the plan type, insurer, and submission method.

- South Carolina: Fully insured group plans must pay or deny claims within 60 days after receiving all required information (Department of Insurance, SC). This ensures timely adjudication and reduces delays for both providers and patients.

- Texas: For secondary insurers, electronic claims must be processed within 30 days if the claim is complete and accurate; however, paper claims have a maximum processing time of 45 days (Texas Department of Insurance).

- Nevada: Insurers are required to:

- Maintain systems to track claim timeliness

- Log the date of receipt for all claims

- Acknowledge receipt within 20 working days

Note: Nevada law does not mandate a fixed deadline for final claim determination.

- New York: If provider contracts do not specify submission deadlines, insurers must still allow a “reasonable” window for claims to be processed, although no specific minimum timeline is established.

These state-level variations underscore the importance of understanding both federal and local regulations, as claim timelines, documentation requirements, and processing expectations can vary significantly by jurisdiction.

Common Reasons Your Claim May Be Delayed

Claims can be delayed due to disputes over responsibility, incomplete information, complex cases, high claim volumes, or missing documents. Recognizing these factors helps policyholders anticipate potential delays and take steps to expedite processing, as detailed below.

- Disagreements Over Cause or Extent of Damage: Claims can be delayed when there is uncertainty or dispute regarding what caused the damage or injury, or the severity of it. Insurers need to verify responsibility and accurately assess costs before approving payment. If negligence is involved, the insurer may deny the claim entirely.

- Incomplete or Incorrect Claim Forms: Claims submitted with missing or inaccurate information require additional follow-up. The insurer must contact the policyholder for corrections or additional details, which naturally extends processing time.

- Complex or High-Value Claims: Claims involving multiple parties, substantial monetary amounts, or unusual circumstances typically require more time to evaluate. These cases require thorough investigation and careful documentation to ensure a fair settlement.

- High Claim Volume: During periods of increased claim submissions, processing times can be longer. Insurers must manage workloads across multiple cases, which can slow down the resolution of individual claims.

- Missing Documentation or Evidence: Certain claims require supporting documents such as police reports, medical bills, repair estimates, or photographs. Without these, insurers cannot complete their review, resulting in delays until the necessary information is provided.

Errors, missing documentation, and manual coding can slow claim approvals and revenue cycles. RapidClaims utilizes AI, machine learning, and NLP to automate coding, detect documentation gaps, and provide real-time insights. Hospitals, physician groups, and billing companies can streamline claims processing, reduce administrative costs, and enhance compliance.

How to Speed Up Your Insurance Claims Process?

You can take several proactive steps to help ensure your insurance claim is processed more quickly:

- Gather All Required Documentation: Before filing a claim, collect all necessary documents, including proof of insurance and evidence of loss or damage. This may include photographs, repair estimates, receipts, and police reports. Having everything prepared upfront reduces delays and streamlines the review process.

- Provide Clear and Concise Information: Describe the incident and its resulting damage in a straightforward and detailed manner. Clear explanations help the insurer quickly understand the situation, minimizing the need for back-and-forth requests for clarification.

- Maintain Receipts and Records: Keep organized records of all expenses related to the loss, including repair costs, replacements, and other incident-related expenditures. Insurers often require these documents to verify and process your claim.

- Submit Claims Promptly: File your claim as soon as possible after the incident occurs. Early submission enables the insurer to begin processing immediately, thereby reducing the likelihood of unnecessary delays or potential denials.

- Consider a Public Adjuster: If your claim is denied or appears underpaid, hiring a public adjuster can be beneficial. These professionals advocate for policyholders, manage documentation, and negotiate with insurers to maximize the claim payout.

Let’s take these proactive measures further by adopting workflow strategies and compliance practices to speed up claims processing.

Best Practices for Healthcare Operations Teams

To improve claim turnaround times and reduce administrative bottlenecks, healthcare operations teams should adopt comprehensive strategies that address workflow, compliance, and analytics:

1. Prioritize Electronic Submissions (EDI)

Electronic claim submission automates verification, reduces human error, and accelerates adjudication. EDI systems also provide immediate acknowledgment of receipt, enabling teams to track claims efficiently and minimize processing time compared to paper submissions.

2. Conduct Thorough Eligibility Verification

Before services are rendered, confirm patient coverage, deductibles, copays, prior authorization requirements, and any policy limitations. Proactive verification minimizes the risk of rejected claims, ensures compliance with payer rules, and allows staff to resolve discrepancies before submission.

3. Ensure Accurate Coding

Correct use of CPT, ICD-10, and HCPCS codes is critical. Even minor coding errors can trigger claim denials or audits, causing significant delays. Investing in coder training, software validation tools, and internal audits can maintain coding precision.

4. Track and Follow Up on Aging Claims

Implement a systematic tracking process for claims that exceed the standard processing window (30–45 days). Timely follow-ups with payers can prevent prolonged delays, uncover missing information, and reduce write-offs.

5. Utilize Denial Management Analytics

Use data analytics to identify patterns in claim denials. Understanding root causes, whether coding errors, eligibility issues, or documentation gaps, enables process improvements, staff training, and payer-specific strategy adjustments.

6. Stay Informed on Regulatory and Payer Update

Health plan requirements, federal/state regulations, and technology platforms evolve continuously. Regular training and monitoring of payer bulletins ensure compliance, optimize submissions, and avoid unnecessary delays.

Implementing these best practices enables healthcare operations teams to enhance claim accuracy, expedite reimbursements, and foster stronger relationships with payers and patients.

Conclusion

While ERISA provides federal timelines for claim processing, 72 hours for urgent claims, 15 days for pre-service, and 30 days for post-service, actual turnaround can vary widely. Factors such as submission method, claim complexity, insurer practices, and state regulations often extend processing times. Awareness of these factors helps providers and revenue cycle teams minimize delays and ensure timely reimbursements.

For faster, more accurate claim handling, platforms like RapidClaims offer AI-driven automation, real-time documentation checks, and seamless EHR integration. By reducing errors, optimizing coding workflows, and ensuring compliance, RapidClaims enables healthcare organizations to accelerate approvals and enhance revenue cycle efficiency.

Streamline your claims, minimize delays, and enhance revenue with RapidClaims. Request a Free Demo today to see AI-powered medical coding automation in action.

Frequently Asked Questions (FAQs)

1. Can claim processing times differ between in-network and out-of-network providers?

A. Yes. In-network providers usually have faster claim processing due to pre-established contracts and standardized forms. Out-of-network claims require additional verification and coordination, which can extend timelines. Knowing network agreements helps providers anticipate delays and manage revenue cycles effectively.

2. How do coding errors affect claim turnaround times?

A. Incorrect or incomplete coding is a leading cause of claim delays. Errors in ICD-10, CPT, or HCPCS codes often result in denials or clarification requests, necessitating resubmissions. Accurate coding upfront reduces processing time and administrative workload.

3. Do electronic claims process faster than paper claims?

A. Generally, yes. Electronic Data Interchange (EDI) claims are typically automated and processed within 7–14 days, whereas paper claims may take 30–45 days. However, even electronic claims can face delays if documentation is incomplete or prior authorization is needed.

4. How does claim bundling affect processing times?

A. Claim bundling combines multiple services into one submission. While it can simplify processing for related procedures, insurers may review bundled claims more thoroughly. Misbundled claims can result in partial payments or delays, making accurate documentation critical.

5. Do high-cost procedures take longer to process?

A. Yes. Claims for high-cost procedures are often subject to additional scrutiny, including medical necessity reviews and utilization checks. These reviews can add days or weeks to standard processing timelines. Thorough documentation is essential to avoid delays.